For more stories like this, sign up for the PLANSPONSOR NEWSDash daily newsletter.

Opinions September 3, 2019

Barry’s Pickings: Meaning for DC Plan Participants of Decreases in Interest Rates

Michael Barry, president of O3 Plan Advisory Services LLC, explains how, in the long run, decreases in interest rates drive up costs for DC plan participants to provide themselves retirement income.

Art by Joe Ciardiello

The last time I wrote about them, medium- and long-term interest rates were about 50 basis points higher than they are now. That was two months ago.

If you think about retirement income as an in-kind benefit, the cost of, e.g., providing $1 of retirement income to a 40-year old went up around 17% in the last two months.

In a corporate defined benefit (DB) plan, this increase in cost is generally (and with a lot of smoothing thrown in) made explicit under generally accepted accounting principles (GAAP) disclosure rules. How is it reflected in a defined contribution (DC) plan?

DB plan sponsors carry three major types of risk—interest rate, asset, and mortality. In a DC plan all three of these risks are transferred to the participant. The significance of this transfer is, with respect to the latter two (asset and mortality (aka “longevity”) risk), relatively intuitive. We all generally understand that in a DC plan the participant is on the hook for asset performance and should somehow hedge against “living too long.”

But what happens—in the shift from a DB to a DC retirement savings model—to interest rate risk? The answer to that question is interesting and a little confusing, in that it points in many different directions at once.

The multiple functions of interest rates

Let’s begin with the fact that interest rates and investment returns are connected, and in more than one way. First of all, interest rates are, among other things, just another form of investment return, which can make treating them as a separate sort of risk a little confusing.

Second, interest rates are a proxy for certainty, in two dimensions. For a corporate DB plan, e.g., they represent a way of (more or less) definitely calculating the value of the DB liability on the firm’s books. Hence their utility as the most transparent version of the plan’s cost to the firm.

But they also are the market return available to an individual who prefers certainty to risk.

Third, changes in rates (holding other variables constant) have a direct effect on equity valuations, more or less on the same principle by which they affect DB plan liability valuations. For instance, a decrease in interest rates will result in an increase in the value of a firm’s stock and (more generally) in the value of the S&P 500.

Fourth, they (fundamentally) reflect the relative supply of lenders/demand for credit and as such are an index of the market’s view-of-the-future. If it’s not clear: very low interest rates reflect a belief that there won’t be a lot of growth in the future.

Fifth, to some extent—I would argue only to a very limited extent and generally only with respect to short-term rates—they reflect central banking (in the U.S., the Federal Reserve Bank) monetary policy. That is, sometimes changes in some market interest rates may have more to do with what the Fed is doing than with the first four factors I have noted.

Much of the confusion about the effect and “meaning” of changes in interest rates reflects the fact that as the factors described above interact, any given change may be associated with totally different results. The simplest example: a drop in rates is sometimes associated with an increase in equity values and at other times associated with a decrease in equity values (typically, reflecting the market’s differing views of expected future earnings).

In the long run, interest rate declines will affect DC plan participants

So, roughly and with a number of qualifications, a drop in interest rates is going to be associated with a write-up of assets (stock and bonds) and liabilities on the books, and a lowering of future earnings expectations (including returns to stocks) and liability growth.

There is a good argument that a DC plan participant is in a better position to take more risk than a DB plan sponsor is—because the participant does not have to publish financial statements that are constantly updated for losses related to, e.g., decreases in the plan valuation rate or losses on the plan’s asset portfolio, or both. Many participants have available to them “Plan Bs”—such as working longer or living on less—that are not available to a corporate DB sponsor. In other words, a DC participant may have a more elastic preference for risk than a DB sponsor and may be able to move further to the right on the efficient investment frontier as the returns to certainty (that is, interest rates) go down.

But—and this is probably the greatest oversimplification in this article—if interest rates go down and stay down, returns on equities will at some point follow.

Moreover, as an individual/participant/retiree ages, his preference for risk shifts to the left—that is, he is less risk-tolerant. If, as many are advocating, the participant—say, when he retires—annuitizes his DC plan account, then at that point he will have to explicitly reckon with the cost of these lower interest rates.

All of which is a really long way of saying that if the drop in interest rates in the last two months increases the cost of a DB plan sponsor to provide a 40-year-old participant with $1 of retirement income by 17%, it will in the long run drive up the cost of that 40-year-old participant to provide herself with $1 of retirement income from her DC plan account by a similar amount.

The question raised by the July-August declines

As I discussed in my July column, much of this is the result of a worldwide decline in the rate of population increase. Fewer people = less future.

The question which, in one way or another, we are all asking, is at what point will these trends stabilize?

The answer from the interest rate markets is: not yet.

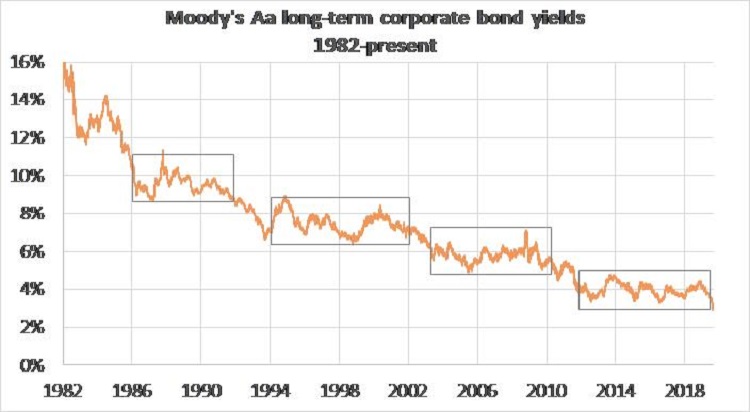

Below is a chart of Moody’s Aa corporate bond rates from their highs in the early 1980s to date.

Sources: https://fred.stlouisfed.org/series/DAAA, https://credittrends.moodys.com/data/bondyields

It seems to me that, looking at this chart, the best Darwinian survival strategy is to think about these rates moving within a window that adjusts over time. So far, that adjustment has been in only one direction: down. If, at any point during the last 35 years, you were assuming that current rates would instead adjust to a (higher) retrospective mean, you would have been wrong.

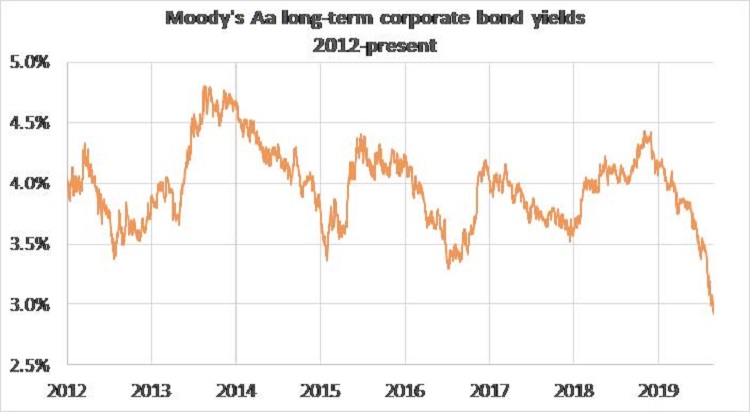

For the last seven or so years, these rates have been moving inside a 3% to 5% window.

The question, at end-of-Summer 2019, is: are we still operating within the “old” 3% to 5% window, or is that window once again shifting down, to a “new” window with lower rates, e.g., 2% to 4%?

Michael Barry is president of O3 Plan Advisory Services LLC. He has 40 years’ experience in the benefits field, in law and consulting firms, and blogs regularly http://moneyvstime.com/ about retirement plan and policy issues.

This feature is to provide general information only, does not constitute legal or tax advice, and cannot be used or substituted for legal or tax advice. Any opinions of the author do not necessarily reflect the stance of Institutional Shareholder Services or its affiliates.