Get more! Sign up for PLANSPONSOR newsletters.

Administration December 22, 2021

Equity in Employee Benefits Communications

Tips to ensure benefits communications reach all employees.

Reported by Karen Witham, DCIIA

Art by Emine Yilmaz

The pandemic has heightened awareness that employees’ unique circumstances affect their engagement with their workplace benefits. Given the upheaval caused by the pandemic, remote working and the “Great Resignation,” now more than ever it is imperative that employers seek to understand who their employees are, what challenges they’re facing, and how to design and communicate about employee benefits in the most equitable and inclusive manner possible.

Here are some tips for employers to ensure their communications reach all employees:

Set the Stage

- Provide internal education to the benefits team and key decisionmakers about implicit bias. Taking quizzes, hosting guest speakers or otherwise discussing implicit bias could prove instructive and help to set the stage for a “learner’s mind,” or an openness to new information and a willingness—indeed, a desire—to learn and grow.

- Question assumptions on any “norms” and whether your communications are inadvertently reinforcing them—whether it be race, ethnicity, age, marital status, education, gender/gender identity, family composition, sexual orientation or otherwise. Are your photos and images inclusive and diverse? Is your language neutral and devoid of outdated metaphors, ideas and terminology?

Review and Refresh Communications

- Consider doing brief, more frequent pulse surveys targeting specific topics, such as whether multiple languages are spoken in the home, any specific accessibility or disability challenges employees may be facing, or other important demographic information that could improve benefits communications. Consider targeting specific employee groups with “deeper dive” questions to gain even more robust understanding of their priorities and challenges.

- Review all employee-facing materials—starting with the job application—to ensure that all language has been updated and is consistent across the board. Is the language clear, concise, inclusive and easy to understand? Are communications visually pleasing and simple to access for employees in all locations and work environments?

- Guard against “headquarters bias,” where employees in the main office(s) get more frequent or better-quality communications than those working in the field, in warehouses or on job sites, or remotely (e.g., desk drops, giveaway items, benefits fairs, etc.). Where possible, seek to be inclusive of all employees, whether it’s leveraging virtual meetings and events, bringing employees to the headquarters, dispatching senior managers on a “benefits tour” or otherwise.

- Create diverse, internal focus groups to test benefits communications and provide candid opinions and insights on an ongoing basis. Ensure senior-level decisionmakers are reviewing the feedback shared in focus groups and surveys and are empowered to act upon it—even incremental changes can help to sustain forward momentum.

Involve the Entire Organization

- Leverage employee resource groups in seeking to create a feedback loop on benefits and lay the groundwork for an ongoing dialogue versus the traditional top-down, one-way messaging. Involve internal experts including the chief diversity officer, marketing and communications, human resources (HR), information technology (IT), and others in planning and communicating benefits.

- Leverage IT resources to the fullest extent possible to help ensure equitable access to information. Consider using apps, text messaging, voicemail messages, internal social networks and more in addition to print, web and email communications. Optimize digital communications using accessibility best practices.

- Collaborate with the IT and HR departments in ensuring employees are receiving all possible support if they face challenges in accessing benefits information due to disabilities or other limitations.

As your program evolves to become more interactive and inclusive, demonstrate that the benefits team is taking employee feedback seriously. For example, “Our April employee survey showed that 45% of our employees speak Spanish in the home and 29% speak Chinese; therefore, starting next month we will be offering key benefits materials in those languages as a standard practice. Employees who need translations in other languages should contact XX for assistance. It is important to us that all employees and their families understand and can take advantage of all of their benefits.” This kind of messaging can help to build the trust that is imperative for employee engagement.

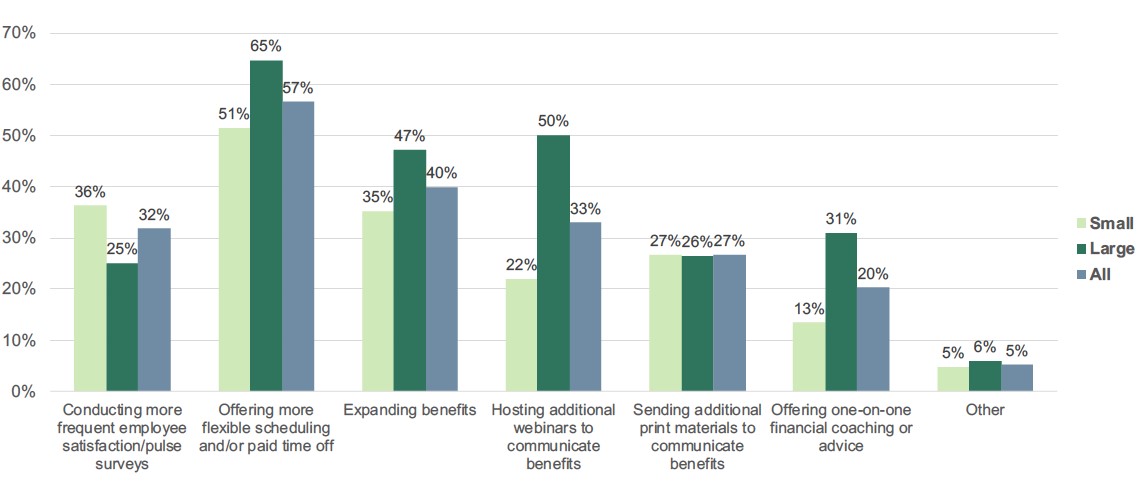

According to the Defined Contribution Institutional Investment Association (DCIIA) Retirement Research Center’s not-yet-published “2021 Plan Sponsor Survey” of 180 plan sponsors, a re-evaluation of employee engagement strategies is already underway due to the pandemic. This chart illustrates recent changes to employee engagement strategies, including employee surveys and benefits communications, broken out by plan size:

Source: DCIIA Retirement Research Center 2021 Plan Sponsor Survey

Key: Large plans are >/=$500 million

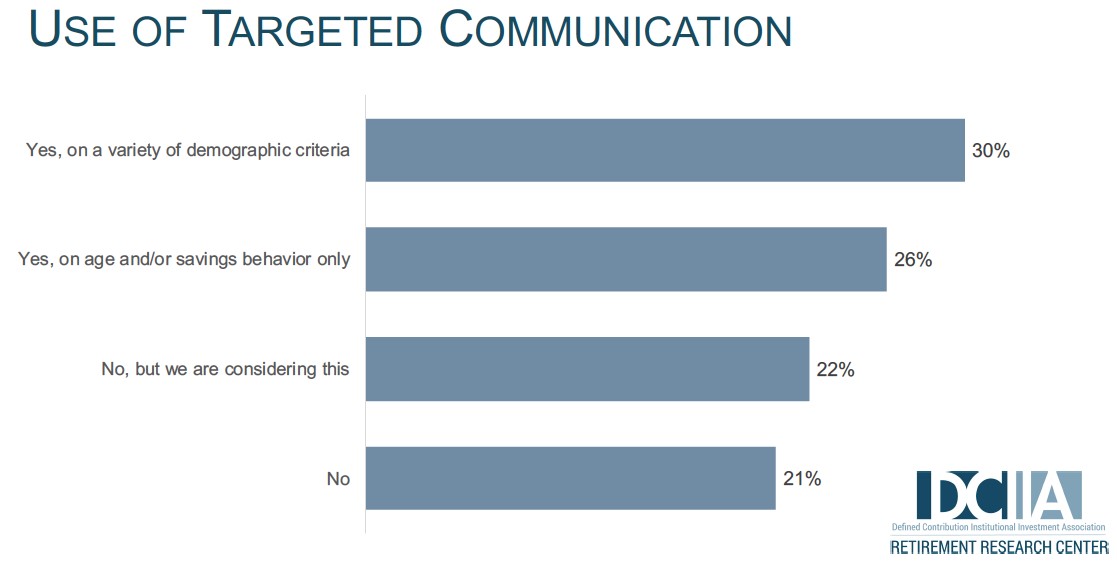

The survey also points to a potential need for plan sponsors to more readily embrace targeted communications, with only 30% of respondents indicating they use targeted communication on a variety of demographic criteria. Targeted communications speak more directly to employees’ unique circumstances and could help to boost engagement with benefits and other positive actions.

Source: DCIIA Retirement Research Center 2021 Plan Sponsor Survey

People’s day-to-day interactions with digital content are increasingly tailored to their interests and personal data. They expect seamless, customized experiences and transactions. Attention spans are shrinking in the face of ever-increasing demands on people’s time. Plan sponsors who are mindful of these trends; who are committed to the principles of diversity, equity and inclusion (DE&I); and who embrace forward-looking best practices and technologies are likely to see positive outcomes in terms of employee engagement with benefits programs, as well as employee satisfaction and retention.

Karen Witham is vice president of communications and marketing for the Defined Contribution Institutional Investment Association (DCIIA) and staffs the communications; diversity, equity and inclusion (DE&I); and environmental, social and governance (ESG) committees.

This feature is to provide general information only, does not constitute legal or tax advice and cannot be used or substituted for legal or tax advice. Any opinions of the author do not necessarily reflect the stance of Institutional Shareholder Services Inc. (ISS) or its affiliates.