For more stories like this, sign up for the PLANSPONSOR NEWSDash daily newsletter.

Administration May 4, 2020

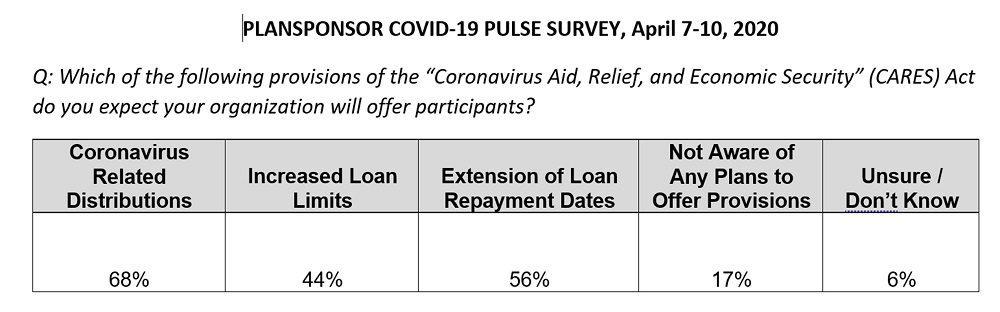

Pandemic May Stall Implementation of Certain DC Plan Decisions

The effects of the COVID-19 pandemic have plan sponsors contemplating what to do about scheduled re-enrollments, the (RFP) process and fund mapping during recordkeeper conversions.

Reported by Amanda Umpierrez

Some defined contribution (DC) plan sponsors that had a re-enrollment scheduled this year have deferred it to later months, Mike Volo, senior partner at Cammack Retirement, tells PLANSPONSOR.

But, not knowing how long the current market climate will last, many plan sponsors are questioning whether and when they should move forward with such plan decisions. The effects of the COVID-19 pandemic on the market and employment arrangements have plan sponsors contemplating what to do not only about scheduled re-enrollments, but also about the request for proposals (RFP) process and moving forward with recordkeeper conversions during which some investments may have to be mapped to new ones.

“In most cases, yes, they should move forward,” Volo says. “But, there is a caveat.” If an employer is planning a re-enrollment process for July 1, for example, the process can continue, he says, but it’s important for employers to add an effective communication plan with an early decision window, along with virtual meetings for education. “That provides participants the opportunity to understand what changes are occurring, and then also allows them to determine their own investment mapping, versus being automatically enrolled,” he explains.

It wouldn’t be surprising if plan sponsors still deferred their re-enrollment process, however. Some may be focused on their employees’ needs first, says Chris Anast, senior vice president and senior retirement strategist with the Retirement Strategy Group at American Funds. Even though he encourages plan sponsors to stick to their long-term plan when implementing changes, postponing could be advantageous when sponsors consider how a re-enrollment could affect participants’ investments. “In this environment, it may be beneficial to just move that off, since there’s so much attention being paid to [the effect on] plans now considering the active market,” he adds.

The RFP process may also need to stall. In a survey for members of the Society of Professional Asset Managers and Recordkeepers (SPARK), conducted in conjunction with the SPARK Institute and DCIIA, RFPs were found to be affected in the wake of the pandemic. Peg Knox, chief operating officer (COO) at DCIIA explains that with most of the employee population working from home, plan sponsors were concerned about managing paperwork, document signatures, payroll and staffing issues, and the lack of “necessary technology infrastructure,” the survey found.

Already scheduled recordkeeper conversions must continue, however. When it comes to fund mapping, Anast says, generally, nothing would change. “You still have an overarching strategy for why you’re making the change and why you’re mapping [to new funds]. Nothing really changes with those ultimate goals,” he stresses. He notes, however, that any investment changes made by participants will change to which funds they will be mapped during the conversion.

Many plan sponsors are pushing back on plan design changes during this time because of market swings, while others are doing so to focus on employees, Knox says. In feedback from employers, Knox notes most were more concerned with helping employees with their current finances than with changing plan design. “There’s this focus on keeping the company afloat and keeping employees employed,” she states.

Still, while studies have found few employers so far are reducing or suspending employer contributions, it’s likely that more will. This may be the most significant plan design change plan sponsors implement this year. Volo reiterates that it’s essential for plan sponsors to carefully consider and provide communication to participants about the change.

He notes that sometimes priorities change, and they especially have during the COVID-19 pandemic.