Get more! Sign up for PLANSPONSOR newsletters.

Thought Leadership June 24, 2013

A Lifetime Strategy

DB-Like Income in the DC Plan

Sponsored by MassMutual Financial Group

Retirement income has been a hot topic in the retirement plan industry for a number of years, and the industry is exiting a phase of talking about it and entering one of action as we see a number of products and services built to assist plan sponsors and plan participants as they prepare to turn their savings into income. On a recent webcast, Charlie Ruffel, founder and director of Asset International, spoke with Tina Wilson, vice president and head of product development for MassMutual Retirement Services about an approach plan sponsors can consider to address the subject of retirement income.

Wilson: Can a defined contribution (DC) plan give participants defined benefit (DB)-like security? Yes, it can. But first participants need to understand the challenge and commit to steady investing. There’s no product or solution that can overcome a lack of savings. Second, make sure that participants have access to effective funding choices, and this refers to the investments in your plan.

MassMutual’s RetireSmart Income Strategy is not a product, and it’s not an investment menu choice. It is a holistic approach that helps participants understand their funding needs so they can create a sustainable income stream throughout retirement.

The benefits of a defined contribution plan are personal control and portability. A DB plan provides a sustainable and steady income stream. MassMutual brings the concepts of the DC and DB foundation together in the RetireSmart Income Strategy, which covers participants from the time that they begin their working lives throughout their retirement and provides professional guidance along the way.

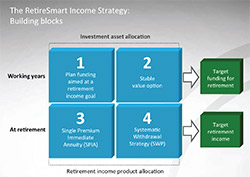

There are four building blocks to the RetireSmart strategy. Two of those building blocks will be the foundation for the working years and are focused on creating target funding for retirement, building up that asset base to create the income stream. The other two building blocks will be the foundation for the retirement years and will create that sustainable income stream.

During the working years, participants need a goal—how much income replacement they will need in retirement and how much of that should be guaranteed. The guaranteed income should cover basic living expenses that will last throughout the participant’s lifetime.

Participants should also look at nonguaranteed income sources—taking managed withdrawals from investments at a conservative rate—to help fund more discretionary expenses and provide liquidity and flexibility.

Block one is plan funding aimed at a prescriptive retirement income goal. Just like a DB plan has an income goal and a funded ratio, the RetireSmart Income Strategy targets a specific income goal. It is critical to measure that goal and show participants how to achieve it. It also requires adequate funding. If the person does not save in his or her plan, the strategy will not be useful.

Block two is creating that foundational piece of the portfolio that becomes vitally important as they move toward retirement. One of the ways that they can do that is to use an age appropriate amount of stable value as part of a balanced asset allocation to create a portion of the portfolio that is not subject to market risk, that has a guaranteed perspective interest rate every quarter and can be looked at to fund the guaranteed piece once they hit retirement.

The strategy is agnostic to the type of stable value product utilized. The key is to have a component of the plan that is not subject to market risk in order to preserve that capital, particularly as the participants get closer to retirement. So, very young people in the plan will have little to no allocation to stable value. As a participant gets closer to retirement, that allocation to stable value increases.

PS: In terms of that stable value option, how do you prescribe that amount? It varies as you come closer towards retirement—are there very specific guidelines on that front?

Wilson: There are, and this whole process comes with guidance. There are different ways to help provide that guidance. It can be done at an individual participant level. As participants go into an online tool, they can put in their preferences. MassMutual’s RetireSmart Ready tool will aggregate all of the financial information provided and present a portfolio that includes an age-appropriate amount of stable value to help fund their future retirement.

Another solution is to create custom target-date strategies based on the investment options available in the plan. A custom target-date can take advantage of the plan’s stable value option, which is probably already in existence and can be used as a qualified default investment alternative (QDIA). You can utilize the plan’s QDIA as a default option for participants who do not make an alternative investment election.

Virtually every defined contribution plan and provider has some array of stable value funds, which limits your exposure to market volatility and provides capital preservation, which is very, very important in those years leading up to retirement.

With professional planning and guidance, the RetireSmart Income Strategy offers participants very prescriptive guidance all along the way; confidence, because they can monitor their progress; and a long-term focus. Advisors can help participants understand those needs, walk them through the tools, answer their questions and help them implement the strategy for their own unique circumstances.

The income strategy is focused on creating a guaranteed level of income, not typically impacted by market fluctuations, and that’s going to be important. But we’re also focused on providing flexibility and liquidity. You need income, and a piece of that being guaranteed, but you also need flexibility and liquidity because there are going to be unanticipated expenses in life. We need to make sure we’re structuring people’s portfolios to handle those possibilities.

Block three is focused on income annuities. These are “plain vanilla” income annuities that have been around for decades. These are tried and true products. For people who need a certain amount of guaranteed income, Social Security and any pension they have may only take them so far—the income annuity provides the rest.

Block four couples income annuities and guaranteed income sources with systematic withdrawal strategies. This is the piece of the portfolio that remains invested in a diverse array of funds or other investment options either in the plan or out of the plan. Having secured guaranteed income for the basic living expenses, participants can actually then employ a conservative systematic withdrawal rate—less than 4%—so that they don’t take too much in any one year and deplete those assets before they are ready.

PS: Are there alternatives that protect against market volatility that you are trying to provide?

Wilson: Sure. A lot of stable value providers in the marketplace have run out of wrap capacity, which means they’ve closed down their stable value options. If you are with a provider that doesn’t have any stable value options, there are other solutions, even a money market account. It’s not ideal in this low-interest-rate environment, but it is not subject to equity market losses.

PS: How can you reconcile this approach with the surge of assets into target-date funds (TDFs)?

Wilson: Not only have we seen a surge into target-date funds, but we have seen an increasing adoption of customized target-date options because of the Pension Protection Act (PPA) and the fact that, as QDIAs, plan sponsors get some protection by defaulting people into these types of investments. Custom target-date strategies meet the definition of a QDIA, can be used in exactly the same way, but a big distinction is, mutual fund target-date structures cannot include stable value because it’s not allowed. In a custom one, it can take advantage of the stable value in the plan. It’s a good solution and still meets the PPA requirements, but also provides that downside protection.

One of the things that we’re watching closely is that, at some point, interest rates will begin to rise. We have been in a 30-plus year secular decline in interest rates. That has provided a lot of benefits to the bond market over time. As interest rates begin to rise, bond prices will be under a lot of negative pricing pressure.

While most target-date funds and mutual funds invest heavily in bonds as participants get closer to retirement, they might get impacted by higher rates, whereas if participants can replace some of their bond allocation with stable value, it provides that downside protection and ultimately, hopefully, a better return.

Even for plans that don’t have custom target-date strategies available to them, they can encourage participants to take advantage of the online tools, guidance, campaigns and whatever other information is available from the provider. That is extremely effective in helping participants understand their retirement readiness, structure their portfolio appropriately and make sure that they’re tracking their funding requirements.

MassMutual’s RetireSmart Income Strategy works by blending that single premium income annuity in the systematic withdrawal strategy to create a much better outcome. We’ve tested these using sophisticated modeling techniques over many, many scenarios and market environments.

By doing this, participants tend to get not only a very good return and income stream but, in some cases, a higher account value. Even though they’re carving off a piece of that balance to buy that income annuity when they hit retirement, because the rest of their portfolio doesn’t have to work as hard, they can actually end up with a better outcome. They have more flexibility and liquidity along the way.

As we evaluated the RetireSmart Income Strategy, we found that the whole is greater than the sum of the parts. These four building blocks together are extremely powerful in not only setting up the participant for success while they’re accumulating assets, but also giving them the confidence and security that they need as they’re drawing income. This is a strategy that can span decades of a participant’s life and is designed to have professional guidance along the way to make sure that they get on track, stay on track and have that confidence throughout the process that they’re meeting those objectives.

It’s focused on how they allocate their assets. When do they start retirement? How do they use guaranteed income solutions? What’s the right amount for them? That answer is going to be different for everybody. What are appropriate annual withdrawal rates for the rest of the portfolio? Part of this solution is providing that guidance around that.

In terms of how you implement this as a sponsor or how you help a sponsor implement this if you are an advisor, step one is to make sure that the plan is structured with the building blocks that they need in order to set up the RetireSmart Income Strategy. If you don’t have a stable value option, the addition can be a powerful tool in securing that income stream.

Investment education is key. Not only do you have to have the foundation there, but also educate people on how to take advantage of it. Structuring a custom target-date strategy that takes advantage of all these components is a straightforward way to do that.

In addition, employee education remains a key piece to this process. Looking at this statistically—we’ve done a lot of work measuring outcomes—we find that two-thirds of the improvement that we can measure, in terms of setting up a participant for success in retirement, is driven by plan design: automatic enrollment, automatic deferral increases and changing the match formula to encourage more savings.

The other third comes from education, but education is not just sending a postcard. It is putting people in the field. It’s having one-on-ones. It’s partnering with advisors.

Step two in the strategy is to motivate participants to fund their DC plan. We have to encourage people that are young, because the earlier participants start, the less they have to save per paycheck. Achieving their goal becomes a whole lot easier by starting early.

Step three is to anticipate retirement decisions before they’re required. We want to educate participants about options before they get to their retirement date, to help them understand what their options are and give them that prescriptive guidance.

In the working years, the RetireSmart Ready tool helps participants understand how much they need to fund and how they should invest. Participants that are age 50 and over now have access to the income component of the tool, which utilizes all of their financial and demographic information and can include a spouse or partner’s information, to provide spend down guidance at a household level. We’re going to show them how much income they can expect to get and how they’re going to get that—what percentage of their income is going to come from Social Security, from a pension plan, from an annuity and from a managed withdrawal. We show them how to set up that managed withdrawal, what the portfolio should look like, the beginning withdrawal rate and how much they need to increase that in the subsequent year.

This strategy is available at no cost, is easy to implement and uses proven strategies that have been around in the industry for decades.

PS: Is there a sense that the market is waiting for the regulators to give the green light to retirement income? Are there parts of the market that want more direction than they have at the moment?

Wilson: With respect to in-plan products, in many circumstances, plan sponsors are waiting because they don’t have the regulatory coverage that they have with target-date funds. But, if you think back before the Pension Protection Act, plan sponsors started to adopt target-date funds because they made sense, and the protection came later. In many situations, I see in-plan income following that same path.

Early adopters for these strategies will drive that change. Once it is accepted from a regulatory perspective, that will be the impetus to truly create a big wave into this space. But with the RetireSmart Income Strategy, because the guaranteed income doesn’t come into play until you are out of the plan, we don’t have to wait for any regulatory coverage on this. We are already in compliance with everything there.

So, it’s one of the other benefits of this strategy. If you put the income in the plan, that’s where, as a fiduciary, you have the concerns. Frankly, we don’t have the regulatory coverage yet. When it’s out of the plan and truly done as a rollover for that participant, I do think that the plan sponsor is more protected.

PS: Where are you in introducing the tool to your client base? Is there a particular segment of the market where you’re being more aggressive?

Wilson: The accumulation version of the RetireSmart Ready tool has been available to all MassMutual participants for more than two years. The income component is the newest component of our Plan Health and Retirement Readiness suite of offerings, and it is available to all participants in the MassMutual product age 50 and older. We’re not targeting any particular size of plan or employer. If you’re a participant in a MassMutual plan, you have access to this key guidance.

PS: Is there a minimum dollar value that has to be in the plan for this to work? Are there minimums that you set?

Wilson: There are no minimums, but the guidance that a participant receives will be altered based on his balance. So, if a participant only has $40,000 in his retirement savings, he will not get an answer that includes any annuity purchase, because an annuity purchase at that rate wouldn’t make sense. That is done automatically behind the scenes in the tool, and there’s logic built for that. So, anyone at any asset level can actually take advantage of these tools.

PS: What sets this approach apart competitively from some of the other things we’re beginning to see?

Wilson: The biggest difference here is that the RetireSmart Income tool can be so customized to the participant’s individual needs and preferences. In an in-plan withdrawal benefit, the investments and the withdrawal rates are the same for all participants of a particular age group. Participants don’t have a lot of opportunity to customize it for their personal needs.

The RetireSmart Income Strategy is meant to be holistic for each participant. Every participant can and should get a different answer based on their unique needs and preferences.

PS: In this environment, what are the metrics, and how do you go about choosing a good stable value option from a plan sponsor standpoint?

Wilson: When doing your evaluation, different flavors of stable value are available, and those should reflect the demographics in your plan. Ultimately, you want to look at whoever is providing the guarantee around the stable value, you want to look at their financial solvency. What are the ratings? What do they have for capital?

The other thing you want to focus on is the rate. How is the rate calculated? What is the guaranteed rate? What has the history been of that rate? That’s going to provide that upside for the participants in the plan.

If your plan decides to eliminate the stable value from its lineup at some point in the future, you should look at and evaluate what provisions are attached to them. Would you be more comfortable with a higher rate if it has a market value adjustment? Would you be comfortable with a lower rate if it had something like a 12-month put?

You should also be aware of different out provisions.

Ultimately, all of us in this industry—whether you’re a provider, a sponsor or advisor—should be focused on everything we can do to improve the retirement readiness and success of participants and plans.

©2013 Massachusetts Mutual Life Insurance Company, Springfield, MA 01111-0001. All rights reserved. www.massmutual.com. MassMutual Financial Group is a marketing name for Massachusetts Mutual Life Insurance Company (MassMutual) and its affiliated companies and sales representatives.

RS: 32079-00