Never miss a story — sign up for PLANSPONSOR newsletters to keep up on the latest retirement plan benefits news.

Thought Leadership August 30, 2017

One Size Does Not Fit All

Selecting and monitoring a QDIA is one of the most important plan sponsor duties

Sponsored by American Century Investments

Diane Gallagher

Selecting an investment to serve as a plan’s qualified default investment alternative (QDIA) is a fiduciary action for which plan sponsors frequently look to their advisers for help. To discuss the role retirement plan advisers play in this selection, PLANSPONSOR spoke with Diane Gallagher, vice president of retirement marketing and value add at American Century Investments. She discussed the need for a process and gave insight as to how plan sponsors might work with retirement plan advisers to make a prudent selection.

PLANSPONSOR: Why should a plan sponsor have a process for selecting a qualified default investment alternative [QDIA]?

DIANE GALLAGHER: Fundamentally, a plan sponsor is a fiduciary and using a prudent process goes hand-in-hand with that responsibility. As you and your readers know, it’s not necessarily about the ultimate choice you made but the process you employed to get there.

With the nearly straight line increase in the adoption of QDIAs following the Pension Protection Act of 2006 [PPA], it’s mission critical for sponsors to take stock of where they are, how they got there and what they are monitoring going forward.

In many instances early on, sponsors only selected a QDIA during a recordkeeping change, or simply defaulted to the recordkeeper’s solution. As the industry has evolved and flows into QDIAs have dominated, it’s become increasingly important to commit to a thoughtful, repeatable process in making and monitoring that QDIA decision. Considering the potential impact on participants’ ability to retire, it only emphasizes that gravity.

The magnitude also demonstrates the need for the expertise of a dedicated retirement consultant to guide a sponsor through that process.

PS: Do you know a success story where having a process like this especially protected a plan sponsor, an adviser or both?

GALLAGHER: We’ve received positive feedback from individuals and organizations who have used this program. The process offers value to the plan sponsor in that they can adhere to a documented process.

PS: What’s the most important element for a plan sponsor in selecting and monitoring a QDIA?

GALLAGHER: Plan participants are key. It’s important to consider participant behavior, engagement level, whether they have access to a defined benefit [DB] plan, and what they historically do with their balances when they terminate employment, among other factors. If the goal of the plan is to help provide a secure retirement for employees and we typically see participants remain in the default, the QDIA selection is an even more critical decision. Again, it’s an opportune time to engage an expert in establishing, following and documenting that process.

PS: What have you developed to help plan sponsors and advisers as they create a process to select and monitor their QDIAs?

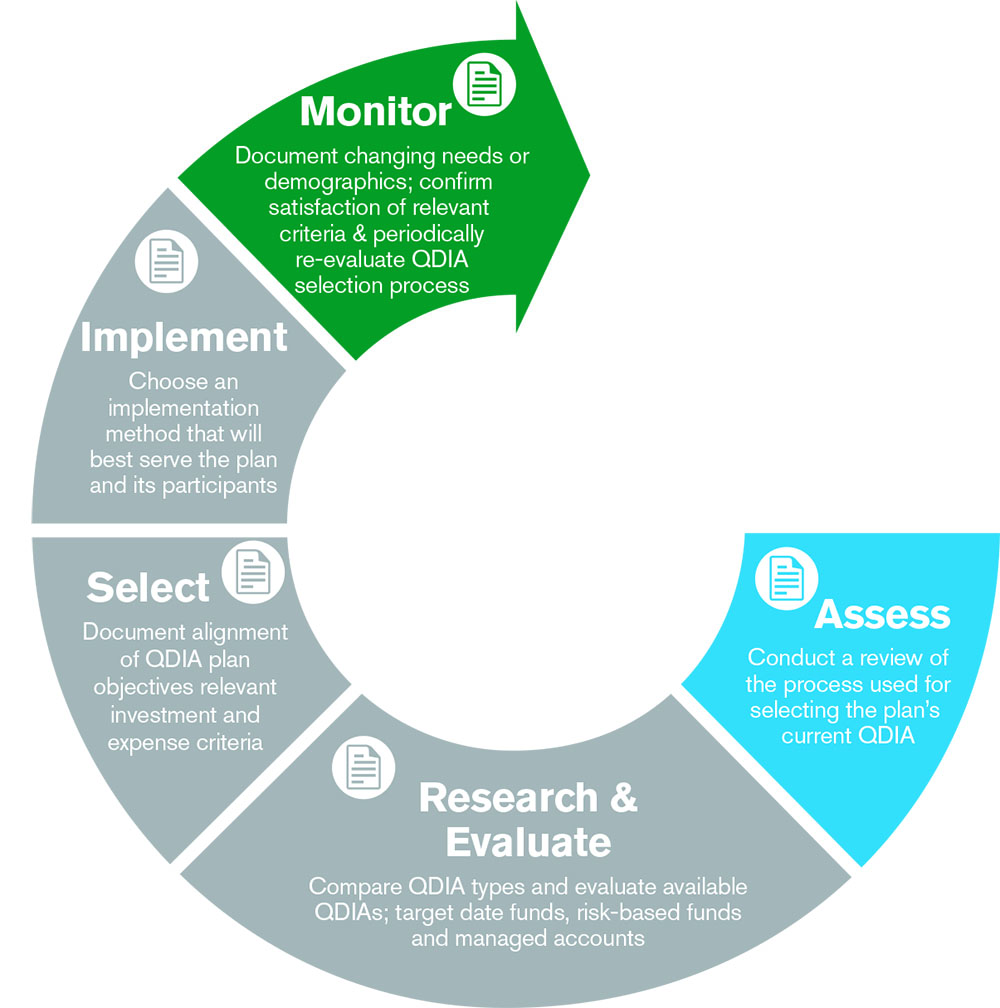

GALLAGHER: We developed a QDIA Selection Process Kit that includes five elements which are (1) a plan sponsor guide, (2) an adviser guide, (3) a discussion guide, (4) an overview of the process, and (5) an infographic of the evolution of QDIA. The materials offer some historical context, considerations around criteria of selection and implementation, monitoring and a road map.

All the materials center on a five-step process: assess needs, research and evaluate available QDIAs, select the QDIA, implement the selection and monitor going forward. The plan sponsor and adviser may work together through the entire process and weigh what’s in the best interests of the participant base.

PS: Then what do you see as the adviser’s involvement vs. that of the plan sponsor?

GALLAGHER: A 3(21) adviser, for one example, offers expertise and a process; he or she walks the sponsor through that process, educates the committee on industry best practices and offers suggestions. Again, the plan sponsor has ultimate responsibility, but often the adviser plays the role of facilitator to help ensure the structure is followed consistently.

PS: How did you develop the program?

GALLAGHER: We partnered with Jason Roberts and the Retirement Law Group to develop the QDIA Selection Process Kit. We wanted to provide objective subject matter expertise to our partners. Jason’s insight, credentials and experience were essential in the key content, and we packaged the materials for easy use by both plan sponsors and retirement advisers.

PS: How does the QDIA Selection Process Kit address the various types of potential QDIAs?

PS: How does the QDIA Selection Process Kit address the various types of potential QDIAs?

GALLAGHER: The kit offers considerations for risk-based investments, target-date solutions and managed accounts, covering all potential options. It was a development requirement to include all available QDIAs and the features of each in light of the specific participant base.

PS: Do you believe this program will help plan sponsors evaluate their demographics and how their plan and participant groups might be better suited for one option vs. another?

GALLAGHER: That is certainly the intention. Plan sponsors may look at their plan in a different light just by asking questions they may not have previously. That is especially true if they made a decision some years ago. The organization may have gone through a merger or acquisition, the participant population may have changed, certain investments may have either been added or removed, or circumstances may simply be different. For example, the Department of Labor’s [DOL] Tips for ERISA Plan Fiduciaries was released in 2013, and if a sponsor hasn’t examined its QDIA through that lens, it may be an appropriate time to do so.

We hope this will also be a valuable resource for sponsors and retirement plan advisers to partner on behalf of participants.

PS: Anything else we should discuss?

GALLAGHER: These last 10 years have gone by in a flash with dramatic changes since the PPA. When we consider the number of plans with a QDIA today and the tens of millions of retirement plan participants invested in them, we can’t underestimate the importance of the decision. A thoughtful, prudent process to choose and monitor the default – that looks beyond performance and fees – is one of the most important responsibilities of a retirement plan professional.

Learn More:http://bit.ly/AmericanCentury

Investment return and principal value of security investments will fluctuate. The value at the time of redemption may be more or less than the original cost. Past performance is no guarantee of future results. This material has been prepared for educational purposes only. It is not intended to provide, and should not be relied upon for, investment, accounting, legal or tax advice. American Century Investments and Retirement Law Group are not affiliated companies. ©2017 American Century Proprietary Holdings, Inc. All rights reserved.