Get more! Sign up for PLANSPONSOR newsletters.

Thought Leadership September 15, 2020

Racial Inequalities in Financial Wellness

To address racial inequalities, we must acknowledge they exist and understand the reasons why. Here, we explore differences by race and ethnicity across budgeting, debt, savings, protection, and financial confidence. While acknowledging historic and continued barriers to financial wellness, we also explore the idea that different priorities shape employees’ finances. Identifying both gaps and successes can highlight opportunities for more equitable approaches to help all employees achieve financial wellness.

Sponsored by Fidelity

Identities influence financial wellness

Identities influence financial wellness

Identities make people who they are, and are made up of visible characteristics, like race, ethnicity and gender, as well as invisible characteristics, traits, and values. Improving employees’ financial wellness requires understanding them beyond their household income, debt, protection, and savings. That’s because identities can shape the opportunities people have, the financial decisions they make, and what financial wellness means to them.

To the right, qualitative interviews with a range of employees reveal how different aspects of their identities directly influence their financial lives.1

In this piece, we focus primarily on race and ethnicity but acknowledge that many other identities—and their intersections—shape employees’ financial wellness as well. For example, Black employees who identify with the LGBTQ+ community may have different priorities and face unique challenges compared to their peers. We are committed to understanding the roles that other identities play in financial wellness.

Please note, throughout this piece we will use “Black” as a reference to both “Black” and “African American” identities and “Latino/a” as a reference to “Hispanic,” “Latino,” “Latina,” and “Latinx” identities. When we refer to “other races” this includes Asian, Native Hawaiian or Pacific Islander, American Indian or Alaska Native, another race, or multiple races.

Level setting on diversity and inclusion

Throughout this piece we will reference diversity and inclusion. Here is how Fidelity defines these terms.

Taking a more inclusive approach to financial wellness

Taking a more inclusive approach to financial wellness

Workforces—and the nation—are growing increasingly diverse, and Gen Z is becoming the most diverse generation in history.2 As they enter the workforce, Gen Z employees may seek employers who take an inclusive approach to their employees’ financial wellness. Employers can benefit by attracting diverse talent through offering modern and inclusive financial benefits programs, and using creative solutions to engage and educate talent.

There’s reason to believe that being “financially well” means something different to different groups. And not all groups place value on the same aspects of finances or go about achieving financial wellness in the same way. For example, a Fidelity study shows that Black, Latino/a, and Asian employees are more likely to have provided financial support to extended family over the past year compared to their white peers.3 Black employees are also most likely to have provided regular financial support to their communities. At the end of the day, this means that employees are supporting the people they care about, but there may be less left over for their own financial wellness.

It’s also critical to understand the historic and continuing barriers that many racial and ethnic groups face that contribute to disparities in financial wellness. Wealth inequality has been a long-standing systemic issue in the United States, making it increasingly difficult for some to achieve “the American dream.” Many factors have contributed to this inequality, including lower than average wages due to limited employment or educational opportunities, reduced access to advantageous workplace retirement savings vehicles like 401(k)s and 403(b)s, and consumer lending policies that may be biased against certain racial and ethnic populations, and subsequently contribute to the widening gap.4,5

Addressing racial disparities in finance isn’t a quick fix. We need to know where there are gaps—and just as importantly, where there aren’t—and understand the reasons they exist so we know how to communicate, engage, and best support employees and close these gaps.

Treating employees as a homogeneous group can make it hard to see who needs the most help

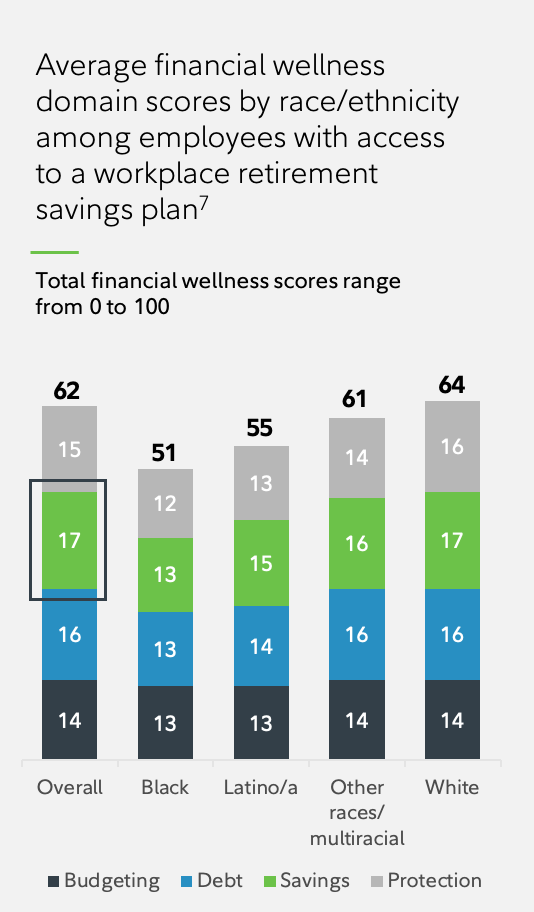

Fidelity research has identified that employees’ financial wellness consists of four key domains: budgeting, debt, savings, and protection.6 Financial wellness includes everything from taking care of the day-to-day all the way to long-term planning, and everything in between.

Among employees with access to a workplace retirement savings plan, 1 in 10 have financial wellness scores that need attention. But among Black employees this is 2.5x higher and among Latino/a employees it’s nearly 2x higher.7 These differences persist even after accounting for differences in household income, suggesting that income disparities are not the only cause. Disparities could be larger among employees without access to workplace retirement savings plans.

Taking a closer look reveals differences by race and ethnicity in some—but not all—areas of financial wellness

The racial wage gap is nothing to be ignored and something employers can take active steps toward evaluating. Yet, even when taking differences in household income into account, Black and Latino/a employees fall short on savings, debt, and protection. These particular disparities could suggest either that existing messaging and solutions on these topics aren’t resonating and/or that they have different priorities that take precedence, such as financially supporting family and community. On the other hand, all groups score similarly on budgeting, suggesting that all employees could benefit from help in this area.

The racial wage gap is nothing to be ignored and something employers can take active steps toward evaluating. Yet, even when taking differences in household income into account, Black and Latino/a employees fall short on savings, debt, and protection. These particular disparities could suggest either that existing messaging and solutions on these topics aren’t resonating and/or that they have different priorities that take precedence, such as financially supporting family and community. On the other hand, all groups score similarly on budgeting, suggesting that all employees could benefit from help in this area.

Communications and solutions should consider the value placed on family and community to better support Black and Latino/a employees with managing debt, building savings, and increasing protection.

Lower levels of emergency savings contribute to more stress about making ends meet

During any financial hardship, emergency savings are key to staying afloat and managing financial stress. Ensuring employees have access to a financial wellness program in their suite of benefits that specifically focuses on debt management and building emergency savings in a way that resonates with individuals’ priorities is a critical first step in closing the financial wellness gap. During the current pandemic, Black and Latino/a employees with access to workplace retirement savings plans were most likely to report increased stress about paying monthly bills—beyond any differences in household income.9 A contributing factor to this increased stress was that Black and Latino/a employees were less likely to have sufficient emergency savings in the first place. On top of that, they were also more stressed than white employees about knowing where to get financial help during this unprecedented time. It’s important to recognize that there were differences in levels of emergency savings before the pandemic hit and these have only been exacerbated by current circumstances. Among employees without access to workplace retirement savings plans, there is likely an even larger disparity in emergency savings.

During any financial hardship, emergency savings are key to staying afloat and managing financial stress. Ensuring employees have access to a financial wellness program in their suite of benefits that specifically focuses on debt management and building emergency savings in a way that resonates with individuals’ priorities is a critical first step in closing the financial wellness gap. During the current pandemic, Black and Latino/a employees with access to workplace retirement savings plans were most likely to report increased stress about paying monthly bills—beyond any differences in household income.9 A contributing factor to this increased stress was that Black and Latino/a employees were less likely to have sufficient emergency savings in the first place. On top of that, they were also more stressed than white employees about knowing where to get financial help during this unprecedented time. It’s important to recognize that there were differences in levels of emergency savings before the pandemic hit and these have only been exacerbated by current circumstances. Among employees without access to workplace retirement savings plans, there is likely an even larger disparity in emergency savings.

Intersecting identities offer a more nuanced understanding of financial confidence

As the workplace grows increasingly diverse, the concept of intersectionality can help us better understand who employees are and the help they need. Intersectionality means that people’s identities don’t exist in a vacuum and that multidimensional identities can result in overlapping disadvantages. Examples of intersectional identities are Black women or biracial men.

Considering multiple identities can also highlight where employees are doing relatively well. Within the context of financial confidence, for example, we can look at the level of confidence reported by men and women with different racial and ethnic backgrounds. Women consistently report lower financial confidence than men, and this gender difference persists across racial groups. However, a closer look at female employees’ confidence in retirement savings reveals areas where certain groups of women are more confident.

With retirement savings, men are still more confident than women overall. But digging a little deeper shows that Black women and Latinas are actually more confident than their white female counterparts. Black male and Latino employees are more confident than their white male peers too, but to a lesser extent. Although Black and Latino/a employees save for retirement at a lower rate than white employees, automated solutions—such as auto enrollment and auto increase programs—may help to close gender and racial gaps in confidence and get employees on the path to longer-term savings.

Equitable financial wellness solutions can result in a more satisfied and productive workforce

Employees with higher financial wellness scores report higher job satisfaction, and this link is strongest among Black employees. A rising tide lifts all ships: leveling the financial wellness playing field may result in lower turnover and higher productivity at work across the board, and especially for Black employees.

Doing our part to eliminate racial inequalities and drive better outcomes for all employees

Be aware of disparities within your workforce

- Consider assessing your workforce to see where there may be racial inequalities in compensation, job opportunities, and financial wellness. Every organization is at a different place in their journey, and there are bound to be inequalities of some form. Taking this leap is an important first step

- Provide safe spaces for your employees to gather, learn, and provide honest feedback on their needs (e.g., Employee Resource Groups)

- Include a financial wellness program in your benefits offering that delivers broad-based financial literacy education, tailored to the values and needs of various communities

Fidelity is committed to doing our part to combat racial discrimination and continue ongoing efforts to create an inclusive experience with a focus on underserved communities.

- Continuing Thought Leadership research to guide the creation of more inclusive experiences and equitable solutions

- As we all work to identify what actions will drive real systemic change, we believe it will be important for the voices of our associates to help guide these actions. This is only a snapshot of our continued journey:

- Doubling down on recruiting efforts to increase hiring of qualified Black and Latino/a associates

- Advocating for Black and Latino/a associates to help advance them into leadership roles

- Through Fidelity Cares, we continue our long-standing commitment of providing financial education to communities, including Title 1 schools, to support school-age children and families with the educational foundation to attain personal and financial success

- Procuring goods and services from minority-owned businesses

- Matching Fidelity associates’ charitable donations to organizations committed to addressing civil rights and social justice issues

Unless otherwise noted:

Covariates included in all analyses are age, gender, and household income, unless otherwise specified.

“Black” includes those who identified as “Black” or “African American” identities.

“Latino/a” includes those who identified as “Hispanic,” “Latino,” “Latina,” and “Latinx” ethnicity, regardless of race.

“Black or Latino/a” references include those who identified as Latino/a (any race), as Black or African American, or both.

“Other race or multiracial” includes those who identified as Asian, Native Hawaiian or Pacific Islander, American Indian or Alaska Native, another race, or multiple races.

1 Fidelity Investments Inclusive Experience, Diversity, Equity & Inclusion research, including 24 focus groups with a total of 115 participants, across diverse groups, backgrounds, cultures, genders, ages, and incomes in three U.S. cities. The focus groups were conducted by CMI® Research, an independent third-party research firm, on behalf of Fidelity in December 2019.

2 Pew Research Center, Social & Demographic Trends, “Early Benchmarks Show ‘Post-Millennials’ on Track to Be Most Diverse, Best-Educated Generation Yet” (November 2018)

3 Fidelity Investments 2020 Financial Experiences Research online survey of 591 FMR LLC employees. Of these, 48 employees identified as Black, 50 identified as Latino/a, and 407 identified as white. The remainder identified as another race or multiracial or did not indicate their race.

4 Angie Beeman et al., “Whiteness as property: Predatory lending and the reproduction of racialized inequality,” Critical Sociology 37 (2010): 27-45.

5 Matt L. Huffman and Philip N. Cohen, “Racial wage inequality: Job segregation and devaluation across US labor markets,” American Journal of Sociology 109 (2004): 902-936.

6 The Fidelity Financial Wellness Score was developed by Fidelity Strategic Advisors Inc., a registered investment adviser and a Fidelity Investments Company. It is based on insight from the Financial Wellness Research Survey of 6k+ active Defined Contribution (DC) plan participants recordkept by Fidelity, who have input into household financial decisions. The score is based on a comprehensive review of the households’ financial situation, including their incomes, spending, savings, debts, insurances, etc. and was conducted in partnership with CMI Research, an independent third-party research firm. July 2016

7 Fidelity Investments Total Well-Being Research online survey of 9,315 active Fidelity 401(k) and 403(b) participants from across the United States. The survey was conducted by Greenwald and Associates, an independent third-party research firm, on behalf of Fidelity in September 2017. 484 employees identified as Black, 622 identified as Latino/a, 6,878 identified as white, 676 identified as another race or multiracial.

8 Total savings rate includes any contributions to DC or IRA, employer match, and spousal contributions (if married/partnered).

9 Fidelity research on market uncertainty from a survey of Americans at least 18 years of age with an investment account. Analysis includes 1,027 workplace investors with a 401(k) or 403(b). The study was fielded from April 1–8, 2020 by ENGINE INSIGHTS, an independent research firm not affiliated with Fidelity Investments. The results of this survey may not be representative of all adults meeting the same criteria as those surveyed for this study. 182 employees identified as Black or Latino/a, 758 identified as white, 87 identified as another race or multiracial.

10 Data represents the Fidelity Investments Health Framework Research online survey of 5,014 employees. The survey was conducted by Greenwald and Associates, an independent third-party research firm on behalf of Fidelity from February 20–March 5, 2020. 1,181 identified as Black or Latino/a, 3,522 identified as white, 300 identified as another race or multiracial.

Financial Wellness Research & Definitions

The Fidelity Financial Wellness Score was developed by Fidelity Strategic Advisors Inc., a registered investment adviser and a Fidelity Investments Company. It is based on insight from the Financial Wellness Research Survey of 6k+ active Defined Contribution (DC) plan participants recordkept by Fidelity, who have input into household financial decisions. The score is based on a comprehensive review of the households’ financial situation, including their incomes, spending, savings, debts, insurances, etc. and was conducted in partnership with CMI Research, an independent third-party research firm. July 2016.

BUDGETING: Spending within one’s means is the foundation upon which financial wellness is built. Maintaining a budget and a positive cash flow are necessary (though not sufficient) precursors to managing debt, saving for the future, investing, and protecting against risk. As a rule of thumb, we suggest spending no more than 50% of after-tax income on essential expenses, such as housing, food, and health care.

DEBT: Carrying too much debt can be a considerable barrier to savings. While all debts pose a burden on financial resources, not all debts are created equal: Some forms of high-interest debt (e.g., credit card debt and payday loans) are particularly harmful because it can be hard to make progress if only minimum monthly payments can be met. Other forms of debt such as mortgages generally have lower interest rates and tax advantages and can be a good way to build credit. We suggest employees carry a debt-to-income ratio of no more than 36% and build a financial plan for paying down high-interest debt (e.g., credit card) as quickly as possible.

SAVINGS/INVESTING: To achieve financial wellness beyond the here-and-now, individuals must not only take control of their debt but also save and invest for the future. This includes long-term savings and investing (e.g., for retirement) but also saving for short-term expenses such as home repairs or vacations. Specifically for retirement, we suggest saving a total of at least 15% of one’s pretax income (combined employee and employer contributions) each year.

RISK/PROTECTION: Financial wellness requires not only managing, accumulating, and investing money appropriately but also insuring against potential losses. Without adequate emergency savings and/or financial protection against catastrophic health shocks, disability, or property loss, one’s financial situation can go from comfortable to distressed in the blink of an eye. We suggest building an emergency savings fund to cover 3–6 months’ of essential expenses and carefully reviewing healthcare and insurance benefits annually to ensure adequate coverage.

For plan sponsor and investment professional use.

Approved for use in Advisor and 401(k) markets. Firm review may apply.

Fidelity Brokerage Services LLC, Member NYSE, SIPC 900 Salem Street, Smithfield, RI 02917 © 2020 FMR LLC. All rights reserved.

943722.1.0

Sponsored by

« Employers Hold the Key to Financial Well-Being in the Age of COVID-19